A fresh new calendar year is underway for capital markets, so much focus is on what we can reasonably expect in the year ahead. But given that capital market movements flow across the beginnings and ends of our calendar pages, it is worthwhile to consider as investors get back up to speed from the holiday season what segments of the markets have been winning thus far, and what areas of the market may have been left behind and offering potential opportunity depending on how events unfold in the weeks ahead.

Winning. With all of the talk about the new calendar year lately, a key date to highlight from recent months is October 30. This is the day that the S&P 500 bounced from its bottom and slingshot to the upside by double-digits through the Thanksgiving and Christmas holiday seasons.

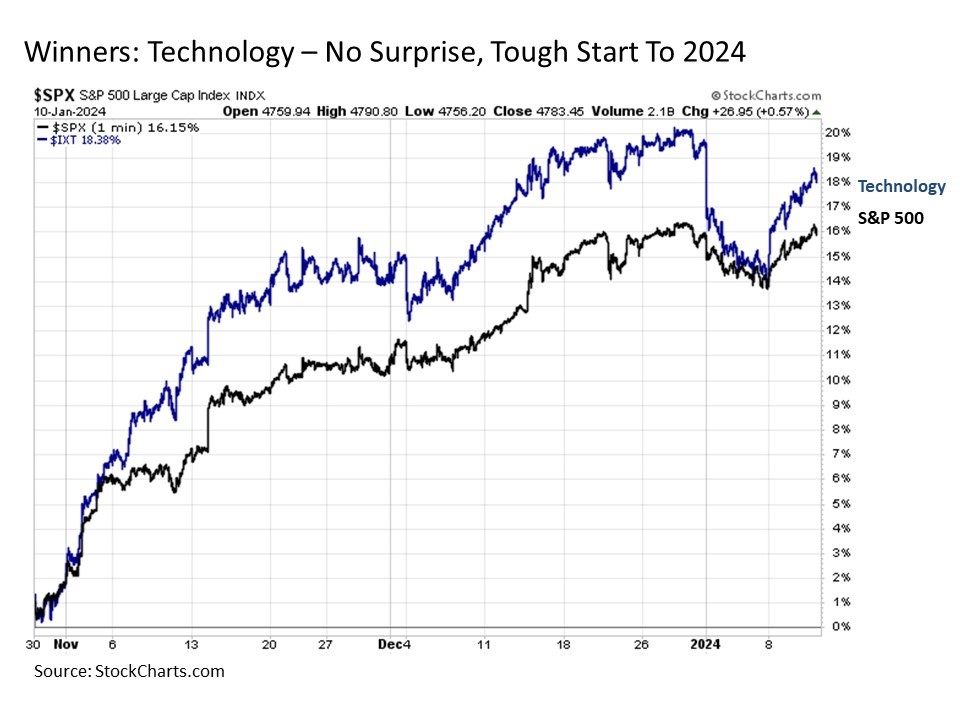

What likely comes as no surprise to investors is one of the primary sectors that has been leading the rally over the past two and a half months is information technology. This sector contains several of the mega cap Magnificent Seven stocks that drove the broader market index higher throughout 2023, and these monster free cash flow generating companies have remained at it through the most recent rally.

It is worth noting, however, that no sector is perpetually invincible, and the tech sector is no exception. Those of us who can remember tech back at the turn of the millennium, financials in the mid-2000s, or for those more seasoned among us the energy sector back in the early 1980s, we know this reality all too well. Thus, the resounding thud from the tech sector at the start of the year, while quickly fading away in the days since, serves as a reminder that even the most persistent market segments can suddenly and swiftly turn to the downside once underlying market conditions change.

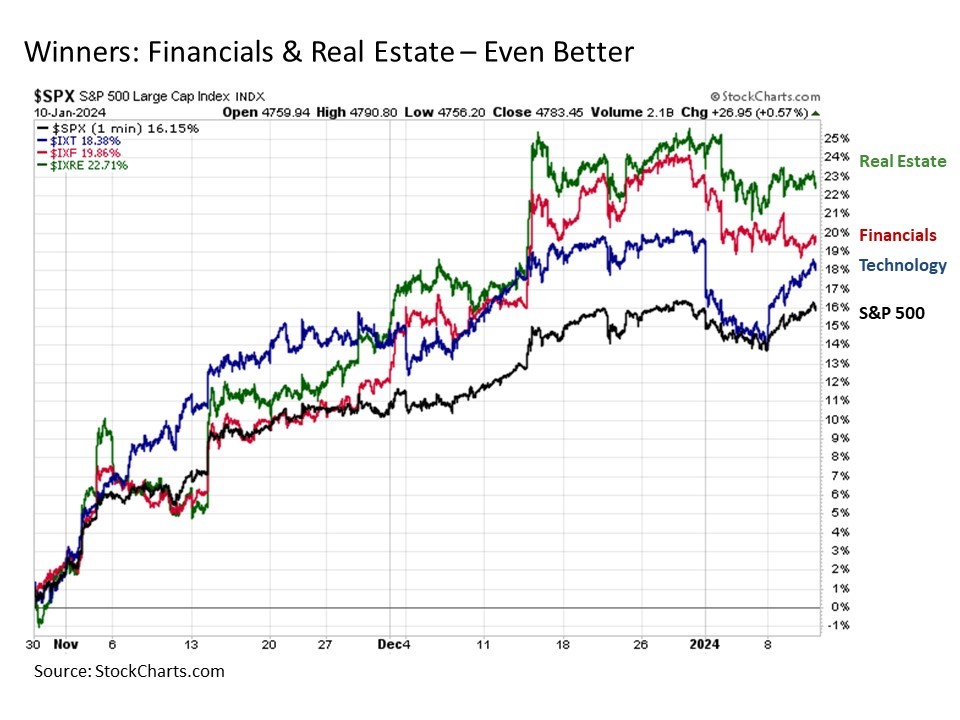

Winning-er. While stocks in general and technology in particular typically dominate all of the financial news headlines, it is worth noting that two other major sectors have performed even better during the most recent market rally since late October. These are financials and real estate.

Of course, it should come as no surprise upon closer reflection that financials and real estate have led to the upside in the latest market rally. Investors have staked their bets during this surge that the U.S. Federal Reserve is not only done for the current cycle raising interest rates (this Chief Market Strategist agrees) but that the Fed may cut interest rates by a quarter point as many as seven times in 2024 (this Chief Market Strategist has a decidedly different view). Given that financials and real estate are highly interest rate sensitive sectors, they stand to benefit most from this bold optimism. Indeed, they also stand to feel more pronounced disappointment if these monetary policy expectations fall short in the months ahead.

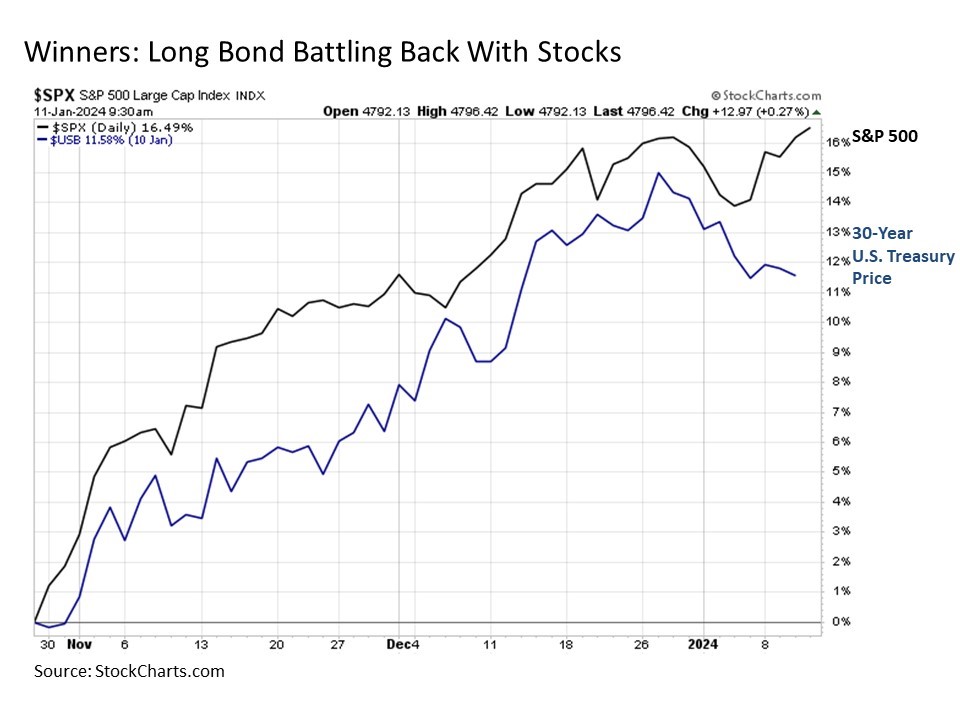

Bond, Long Bond. Speaking of interest rate sensitive investments, the bond market has also seen recent euphoria in part associated with the steady decline in inflation pressures coupled with expectations of easier monetary policy from the Fed in the year ahead. And knowing that the longer the duration of a bond, the more it trades like a stock, we see that the price on the 30-Year U.S. Treasury Bond has rallied almost as strongly as the S&P 500 since the late October rally got underway. This highlights the total return benefits that can come to your portfolio not only within the stock market but also across the asset allocation spectrum.

Calling all contrarians. OK. This all sounds great if things play out as the consensus expects. But what if things play out differently? What if inflation stops continuing to go down? What if an unexpected supply chain disruption or geopolitical event causes inflation to suddenly start sustainably rising again? What then?

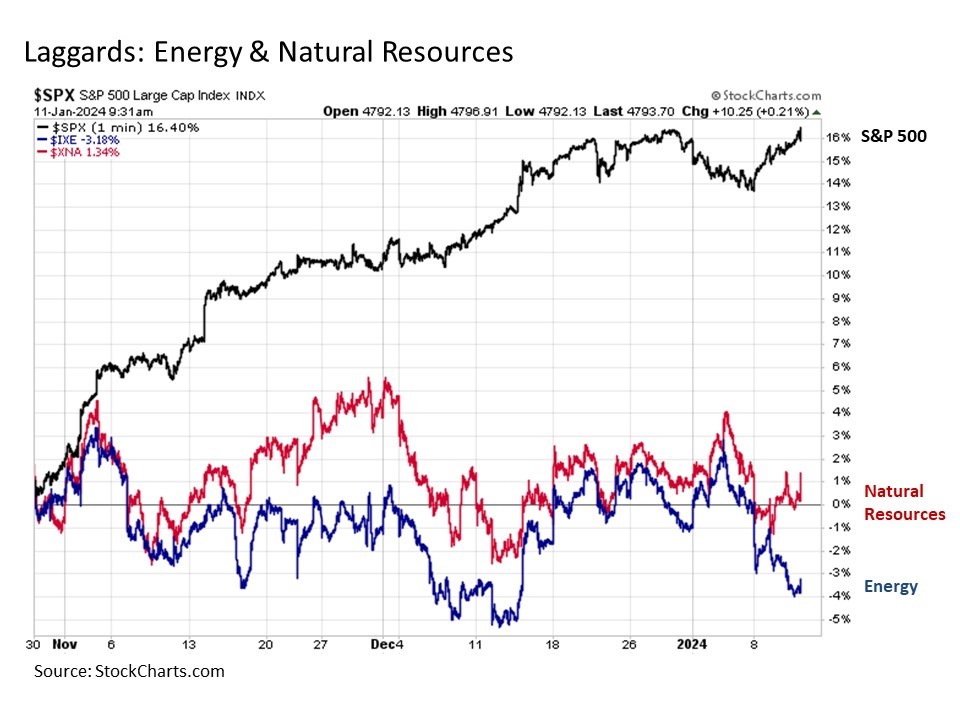

For considerations like these, it is worthwhile to sift through the rubble and identify those areas of the market that have been left behind during the most recent market rally. Leading among these is the natural resources segment generally and the energy sector in particular. Not only are natural resources barely positive, but energy stocks are down by more than -3% at a time when the S&P 500 has rallied more than +16%.

Why focus on this laggard in particular? Because they have likely underperformed in large part under the consensus expectation that inflation will continue to fall an Fed interest rates will soon come down aggressively. But if it turns out that inflation starts to rise anew and/or the Fed is compelled to resume raising interest rates further, these recently beleaguered segments of the market stand to benefit most.

Bottom line. While the investor focus is understandably on the twelve months ahead with 2024 getting underway, it’s just as worthwhile to reflect over the past three months to consider the return potential and risks that we may see in the weeks ahead.

Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article. Investment advice offered through Great Valley Advisor Group (GVA), a Registered Investment Advisor. I am solely an investment advisor representative of Great Valley Advisor Group, and not affiliated with LPL Financial. Any opinions or views expressed by me are not those of LPL Financial. This is not intended to be used as tax or legal advice. All performance referenced is historical and is no guarantee of future results. All indices are unmanaged and may not be invested into directly. Please consult a tax or legal professional for specific information and advice.

Compliance Tracking: #526868-1